TL;DR bringing new assets onto the blockchain is going to result in trillions of dollars of new liquidity, potentially revolutionizing not only DeFi but the way individuals, businesses, and governments manage their finances.

In a recent SKALE Partner Highlight blog, we were asked how we saw DeFi evolving in the next three to five years.

That length of time is an eternity in a space that has existed for less than five years in the first place (DeFi as a movement took shape in the summer of 2018), and making those kinds of predictions has a habit of looking dated really fast. On the other hand, we’ve been active in DeFi sector since it started, in crypto for years before that, and we like a challenge, so we’ll take a shot.

The SKALE post wasn’t enough space to unpack our thoughts fully, so we’ll go into a little more detail in several long-form articles that each explore a particular aspect of what we expect DeFi and Web3 to deliver in the coming years, how we think that will happen, and what role platforms like Ruby and SKALE will likely play.

First up: Liquidity.

Assets Old And New

To state the obvious: Liquidity is the life blood of DeFi.

In the land of DeFi, assets exist on the blockchain and have known supply, alterable only through pre-ordained rules enforced by the network as a whole. Assets are real, in a way that doesn’t hold true through the looking-glass in the so-called “real” world, where financial sleight of hand rearranges the ledgers at the whim of central banksters and corporate clowns.

In DeFiLand, every borrower requires a lender, every seller requires a buyer, and collateral is king. Without collateral—aka real assets—there can be no liquidity.

Right now, liquidity is in short supply. 2022’s catalog of hacks, scandals, and 80-90% drawdowns is dissuading holders from putting funds on the line for the relatively low yields currently on offer.

But even if that wasn’t the case, there’s only a limited amount of liquidity available. Crypto as an asset class has a roughly trillion-dollar total market cap. As things stand right now, only a few tens of billions of dollars at most will ever be locked in DeFi protocols, imposing a fundamental limit on the amount of borrowing, lending, swapping, and other financial activities that can take place.

Fortunately, change is a-coming. The months and years ahead are going to see a wave of new asset types becoming available to blockchain-based protocols, massively augmenting the liquidity that crypto assets themselves will provide (even at the vastly higher valuations everyone hopes to see).

In the world to come, liquidity will come from at least three different sources:

- First-gen crypto assets (BTC, ETH, etc)

- Tokenized TradFi assets (stonks, bonds, commodities, and the other regular suspects)

- New crypto-native assets (particularly weird and wonderful NFTs)

First-gen crypto assets need little introduction. We trust that, if crypto has any legs at all, we will at some point in the not-too-distant future see ETH and BTC hitting all-time highs, with other quality assets rising in line with that (and a lot of junk being heaved unceremoniously into the big crypto dumpster). While that would be nice for HODLers, it won’t be nearly enough to unleash DeFi to do what it really needs to do. For that, we need…

Real-World Assets (RWAs)

Real-World Assets are the ones that are going to unlock a tsunami of new liquidity for DeFi. Global equity is a $120 trillion market, with the S&P500 alone representing over $30 trillion of that. The bond market is comparable, while the forex (currency) markets dwarf them both. Gold is a $12 trillion asset class, and real estate adds several trillion more. Crypto, by comparison, is a minnow.

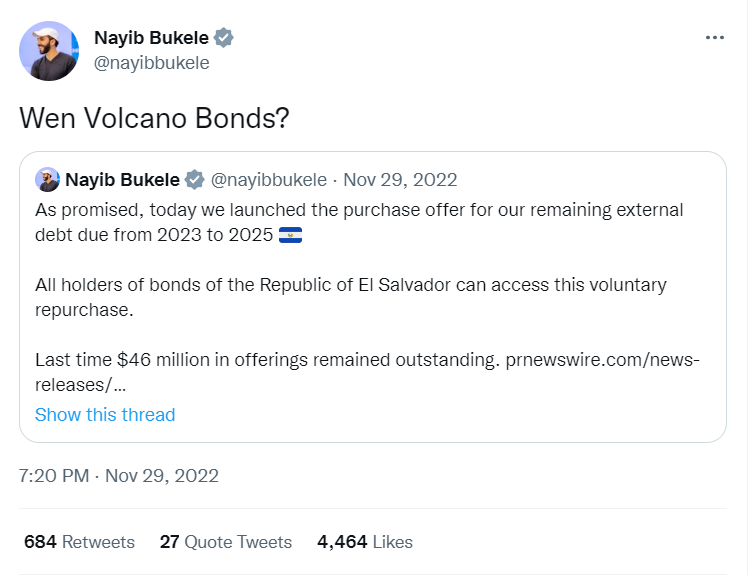

All of these assets are well-suited to tokenization. It’s already possible, of course, to hold dollars or gold on the blockchain, and the first tokenized bonds have been trialled. El Salvador hopes to lead the way with their tokenized Bitcoin bonds. It won’t be so much longer before equities and a bunch of other stuff follows.

Putting RWAs on the blockchain has important and intriguing effects, both for DeFi and TradFi assets. Most obviously, it will turbocharge DeFi adoption by providing that desperately-needed liquidity. We trust that the day will come when you’ll be able to manage your “real world” portfolio on Ruby, adjusting your relative allocations of global stock indices, bonds, et al, all frictionlessly and with zero gas fees. But it will—necessarily—also change the way that TradFi assets are used. In the process, it has the potential to revolutionize household economics.

Moving assets onto the blockchain means they can be used as collateral in ways that simply aren’t possible right now. Let’s say you own a stack of Krugerrands but no cash, and you need money for food, rent, a new computer, bail, whatever. Your only real option is selling some gold—a process that will entail transport and security headaches and costs, slippage, potentially capital gains tax, and the emotional and financial pain of losing an asset you expect to rise in price over time.

If that gold happens to live on the blockchain, you have another option: Borrow against it using a lending protocol. In a mature DeFi ecosystem you will always be able do that because, in a trustless world, collateral is king. The only reason that TradFi lenders are prepared to give you an unsecured loan—assuming they are prepared to give you one at all—is because they make it their business to invite you into the consulting room, don their rubber gloves, and find out a lot about you. In DeFiLand, the lenders don’t need to know your blood type, inside leg measurement, and unredacted internet search history. They just need to know you have collateral.

TradFi assets aren’t composable like this, at least not with anything like the same degree of ease, accessibility, transparency, and efficiency. Holding assets on-chain actually strengthens the case for owning gold, stocks, and so on, rather than keeping a chunk of cash lying around and shrinking with inflation, because you can draw value against that if you ever need to.

This just covers the most obvious and popular of traditional assets. You can of course add tokenized derivatives, and exotic things like invoice receivables, royalties streams, and a bunch more.

And then, of course, there are NFTs.

NFTs

NFTs are going to form a huge part of Web3 and, by extension, DeFi. Notwithstanding the hype around them, their importance is still under-appreciated. Give it a few years and they’re going to be everywhere. They’re going to be your avatars, your passwords, your keys, your financial assets, your identity—basically your online life will depend on them.

The first killer use case for NFTs was collectibles. While NFTs definitely won’t be limited to that, digital collectibles aren’t going away, and have already formed a solid foundation for other use cases—not least online identity. Just think of the way users display prized NFTs as PFPs and status symbols on social media, and how specific NFTs or collections are used to grant access to other communities and opportunities.

It’s quite possible that in the future, physical collectibles will be seen as unusual—at least in terms of their percentage of total collectibles—if not quaint, indulgent, and possibly even immoral. Consider how we view ivory artifacts today: Items that have value and heritage, of a sort, but not exactly something to boast about. They’re the kind of thing an aging aunt might display in her home, in defiance of qualities like taste.

At some point, and perhaps sooner rather than later, it might seem strange that we satisfied our fascination for scarcity by digging fossilized organic matter out of the ground, processing it into sundry objects in energy-guzzling factories, and then plonking the results on shelves for a few years before consigning them to landfill, where they will spend the next several centuries stubbornly refusing to decompose.

Once you’ve conceded the point that digital assets and services are just as real, valuable, and important as their physical counterparts (ProTip: The dollar isn’t backed by gold any more, and the world kept turning when a large proportion of employees went to work via Zoom, instead of by car), it’s not such a stretch to see how digital collectibles are going to take off. Why bother going to the lengths of manufacturing and storing awkward, breakable, easy-to-forge, hard-to-trade objects when digital assets of cryptographically unquestionable scarcity and provenance can be minted, held, displayed, and traded online with minimal cost or inconvenience? Even if you don’t understand it (perhaps you’re also the kind of person who finds yourself shouting at kids to get off your lawn), surely reducing the unsustainable amount of disposable tat we create is laudable?

Anyway, we digress.

In addition to “pure” collectibles, there are what we’ll call utility NFTs. These could be just about anything that have some kind of functionality. That could be access to a game, a community, or a content subscription; or something more explicitly financialized, like bespoke bonds, rent payments for specific properties, a royalty stream from music sales, a share of NFT trading fees, or one of Ruby’s sparkly gemstones.

Naturally, there’s nothing to stop collectible/PFP NFTs serving as utility NFTs, and vice versa. A classic car is both a financial asset and a symbol of status/identity. A platinum-tier credit card is both useful and carries social cachet. A financialized NFT that is also a piece of unique artwork that signifies membership of a particular community and can easily be displayed and linked to your online and/or offline identity serves a similar purpose.

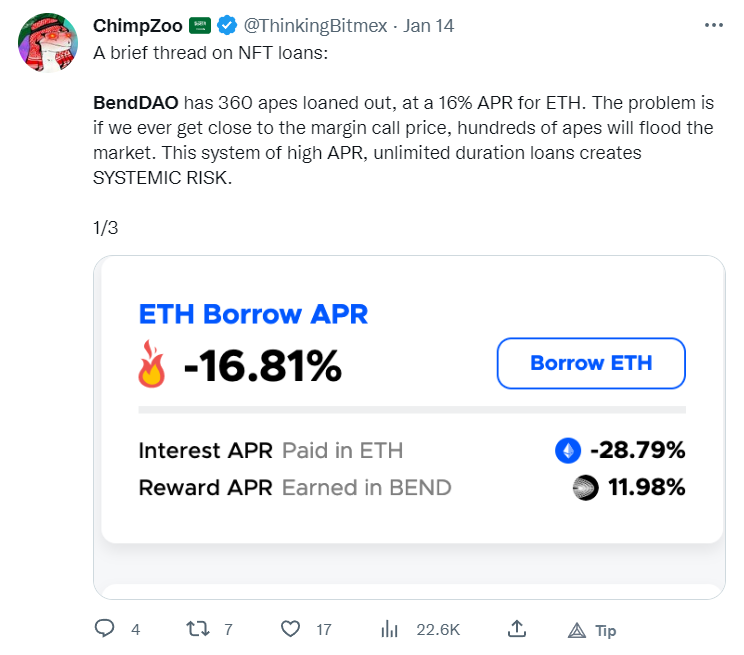

Collectible NFTs can be and are used as DeFi collateral today, but it can be risky. With limited supply, emotion-driven markets, and a lack of fundamentals on which to value them, even blue-chip NFTs can be illiquid—meaning that in the event of a crash, there’s a good chance of bad debt being incurred. In a cratering market, it’s miserable enough to be chasing prices downwards when you’re selling liquid collateral like ETH. With NFTs, you face the possibility that there simply aren’t any bids at all—a problem BendDAO encountered back in August 2022, and that reared its head again recently.

Improved auction mechanics are part of the solution. Utility NFTs introduce fundamental value—through revenue streams or subscription to a service that is worth a certain sum, or some other quantifiable mechanism—are another. Once markets are more mature, what we might very well see is users bucketing together NFTs they have bought, earned, and developed across Web3 apps, and borrowing funds against them, in much the same way as the gold owner does in the example above. Maybe you’re a gamer who has earned a small portfolio of P2E NFTs that you don’t want to sell, but you want some cash to buy another NFT that will provide access to another game with better earning potential. Assuming there’s an active market for your existing tokens, it should be safe to use them as collateral.

As a side note, it only makes sense to put a collection of $10 NFTs up as collateral if you’re not paying gas—which happens to be another subject in the series.

Liquidity Event

All of this has the potential to unlock huge tranches of value that are currently inaccessible—either because these assets cannot easily be used as collateral in their current form (such as shares held with a conventional broker), or because there currently exists no mechanism for trading them at all (e.g. rental income for a bespoke property portfolio).

It doesn’t feel like an exaggeration to say that this would mark a fundamental shift in the global economy. It’s a massive liquidity event that gives individuals, households, businesses, and even governments new tools to manage their finances. At a time when inflation is into double digits and households are facing their biggest squeeze in living standards for a generation, it feels like a meaningful change could be coming.

There are potential downsides, of course. Putting your share portfolio at risk of liquidation by treating it like an overdraft isn’t ideal. But then, there are also risks entailed in having zero cash savings and maxing out your credit cards at 20% APR or more. Consumers can be protected by minimum collateral requirements, hefty safety buffers, risk management tools and, dare we say it, regulation. In any case, if the only alternative is to sell your assets anyway, what’s to lose?

Unfortunately, DeFi is unlikely to come of age soon enough to offset the effects of the current economic crisis. The next one? Maybe.

Follow Ruby on Twitter, join the conversation on Discord, and subscribe to our blog for regular updates.